The First AI Guardian, Built For Us

Build money habits.

Make confident decisions.

Own tu futuro.

Build money habits.

Make confident decisions.

Own tu futuro.

Feeling lost in a financial system that wasn't built for you and doesn't speak your language?

Learn the money habits to build your credit and master your budget.

Gabriel Money is the simple, judgment-free app guide to the future you deserve.

Feeling lost in a financial system that wasn't built for you and doesn't speak your language?

Learn the money habits to build your credit and master your budget.

Gabriel Money is the simple, judgment-free app guide to the future you deserve.

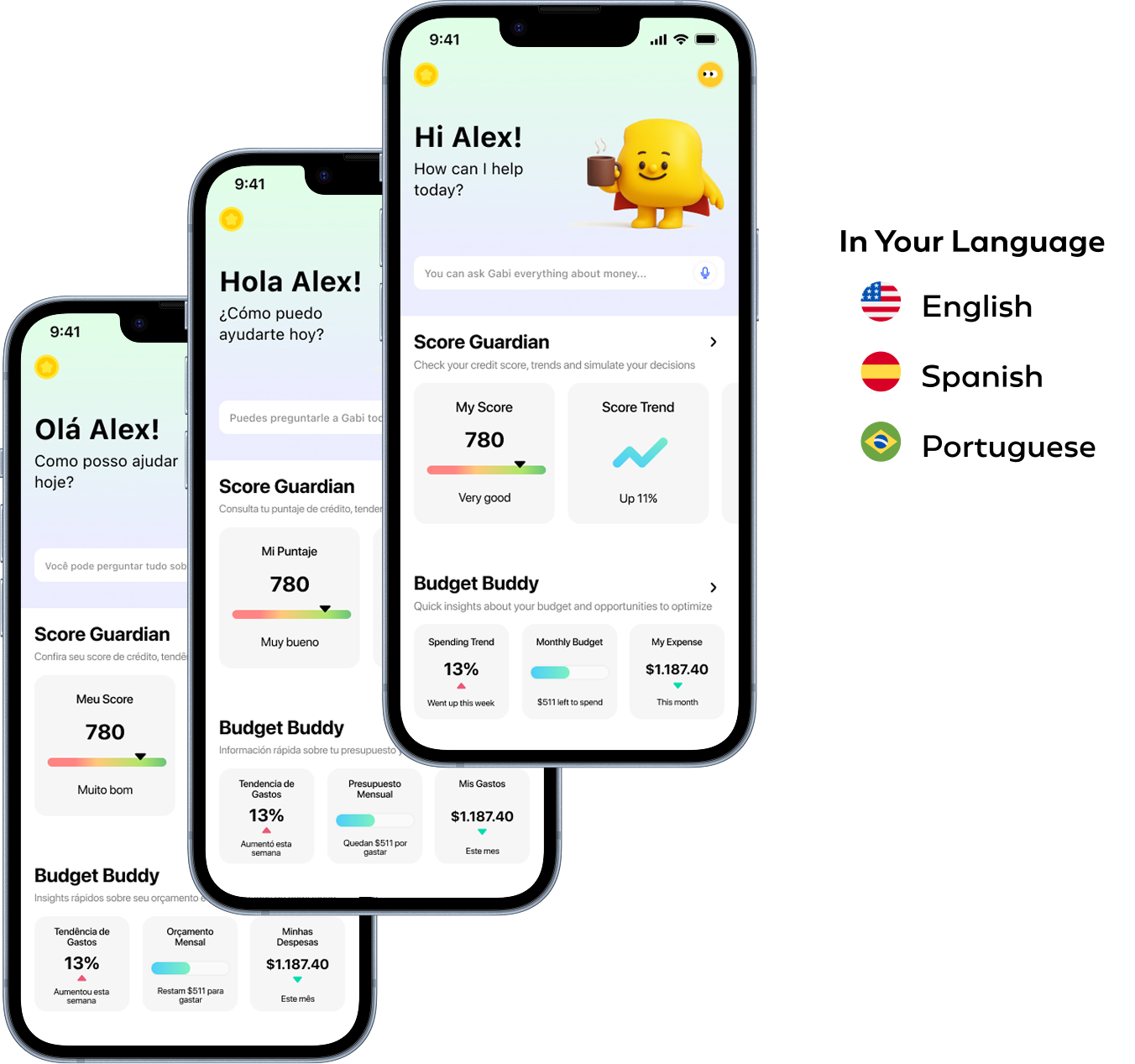

Your private judgment-free AI to navigate your money questions, en tu idioma.

Build

Your Credit with Confianza.

Finally See Where

Your Money Goes.

Get Rewarded for

Learning.

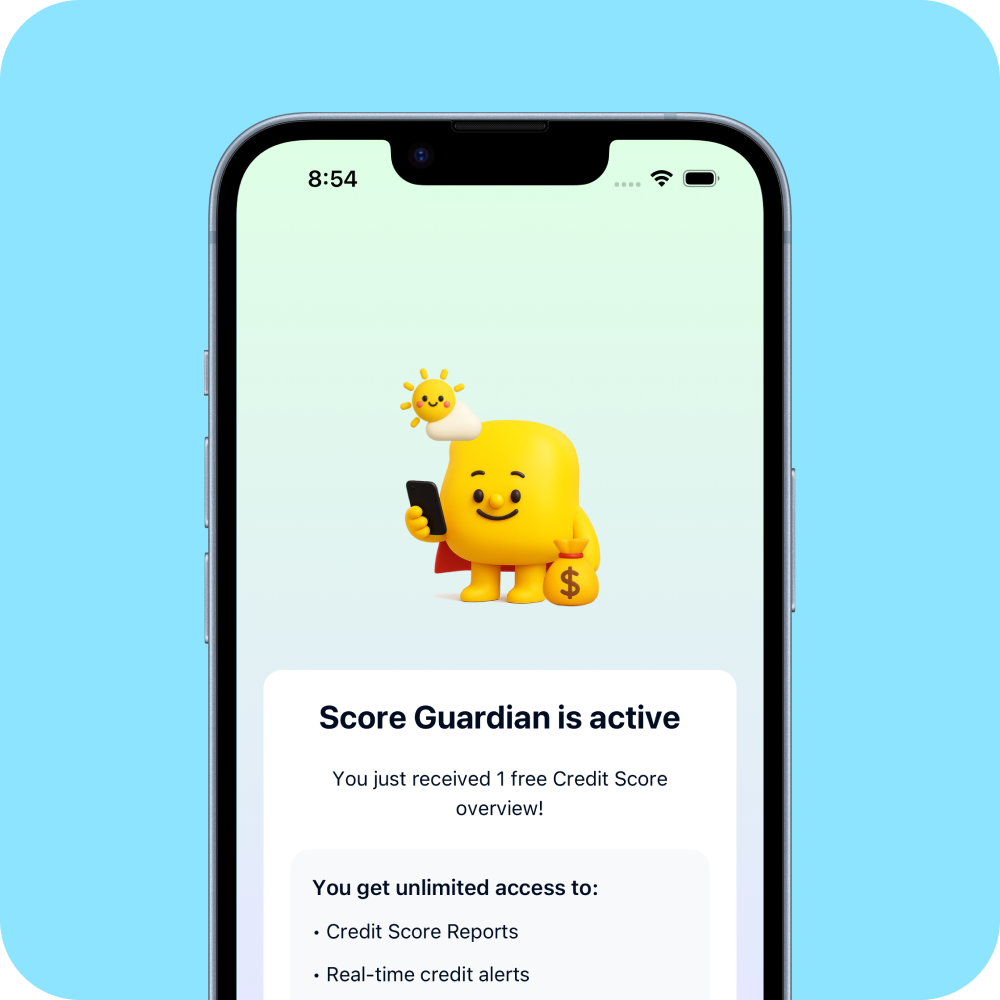

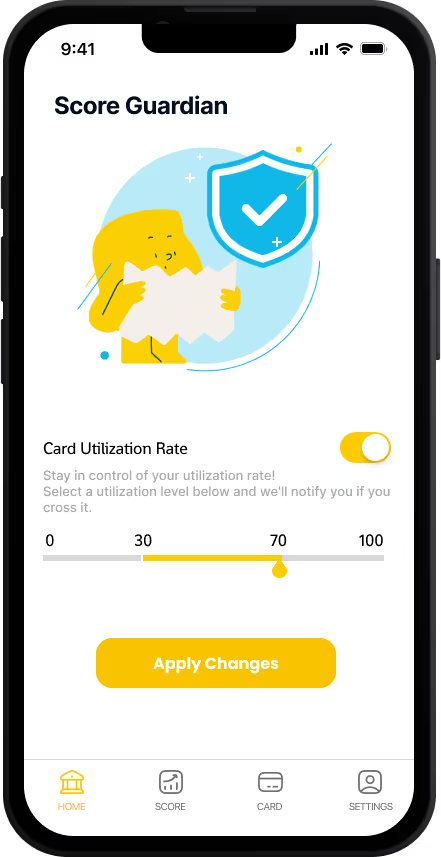

Follow Gabriel's step-by-step guidance to a better credit score.

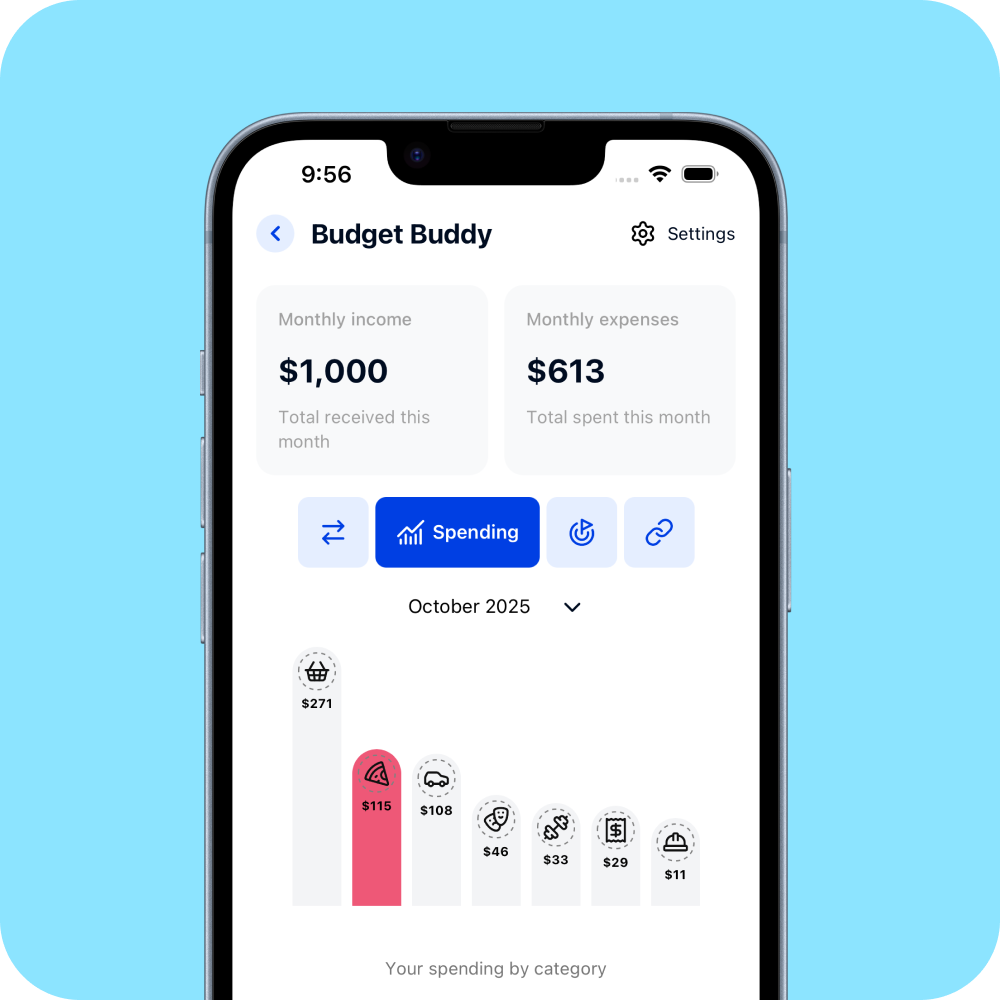

Gain the clarity to create a spending plan that works para ti.

Answer trivia and complete missions to win real prizes.

Build

Your Credit with Confianza.

Finally See

Where

Your Money Goes.

Get

Rewarded for Learning.

The smart way to build credit and take control of your money.

Gabi: AI –

Financial Guardian

Exclusive Services

Advanced encryption technology

We adhere to leading security standards such as PCI-DSS. Additionally, Mastercard’s Zero Liability Protection keeps your transactions safe.

Exceptional customer support

Our dedicated support team is available to assist you with any inquiries or concerns, providing personalized human support.

Control at your fingertips

Lock your card instantly through the app. Enable smart notifications to monitor your finances and log in securely using FaceID.